What is KYC? Meaning, requirements, and how it works [Video]

- azakaw

- Apr 10

- 14 min read

Updated: Apr 30

If you’ve opened a bank account, signed up for a fintech app, used a cryptocurrency exchange, or applied for a mortgage, you’ve already completed a KYC verification process.

Know Your Customer (KYC) is the identity-verification process businesses use to confirm customers' identities before and during a business relationship. It helps organizations prevent fraud and detect financial crime risks, and comply with anti-money-laundering (AML) regulations.

In this article, we provide detailed information about the practical meaning of KYC: the identification procedure, the required documents, the differences between KYC and AML, the role of e-KYC in ushering in a new dawn, and the consequences of failing to provide good KYC. Let’s dive into it!

KYC Key Takeaways |

|

|

|

|

|

|

|

|

|

|

|

|

What is KYC (Know Your Customer)?

KYC (Know Your Customer) is the process businesses use to verify a customer’s identity before and during a financial relationship. It ensures organizations understand who they are dealing with and helps them assess financial crime risk.

KYC forms the foundation of AML compliance programs and allows regulated businesses to:

confirm customer identity

evaluate risk exposure

detect suspicious behavior

comply with regulatory obligations

prevent misuse of financial systems

Banks, fintech companies, crypto exchanges, law firms, accountants, and real-estate professionals typically perform KYC checks before onboarding customers.

Why is KYC important?

KYC is not only a regulatory requirement. It helps organizations prevent financial crime, strengthen governance standards, and maintain transparency when working with customers, investors, and financial partners.

Strong KYC procedures support safer financial systems and reduce the risk of businesses being exposed to illicit activity.

Preventing fraud and financial crimes

Activities such as money laundering, terrorist financing, and fraud rely on anonymity.

KYC acts as a means of dealing with any anonymity. Through identity verification, conducting sanctions screening, and identifying politically exposed persons (PEPs), which prevents illegal activities such as using our company to channel illicit funds.

According to the United Nations Office on Drugs and Crime (UNODC), between $800 billion and $2 trillion is laundered each year globally through financial systems with weak customer due diligence controls.

Regulatory and legal commitments

Financial institutions must follow international compliance standards established by the Financial Action Task Force (FATF) and national regulators, such as:

Financial Conduct Authority (FCA)

Financial Crimes Enforcement Network (FinCEN)

Monetary Authority of Singapore (MAS)

UAE Central Bank

The European Union’s Anti-Money Laundering Directives (AMLD) require organizations operating within Member States to implement effective KYC procedures.

Failure to comply with these requirements may result in regulatory enforcement action and financial penalties.

Creating good governance and transparency

Effective KYC systems demonstrate strong corporate governance and help organizations build trust with financial institutions, investors, and business partners.

Companies that maintain transparent onboarding procedures are better positioned to manage regulatory risk and meet the expectations of stakeholders operating in regulated markets.

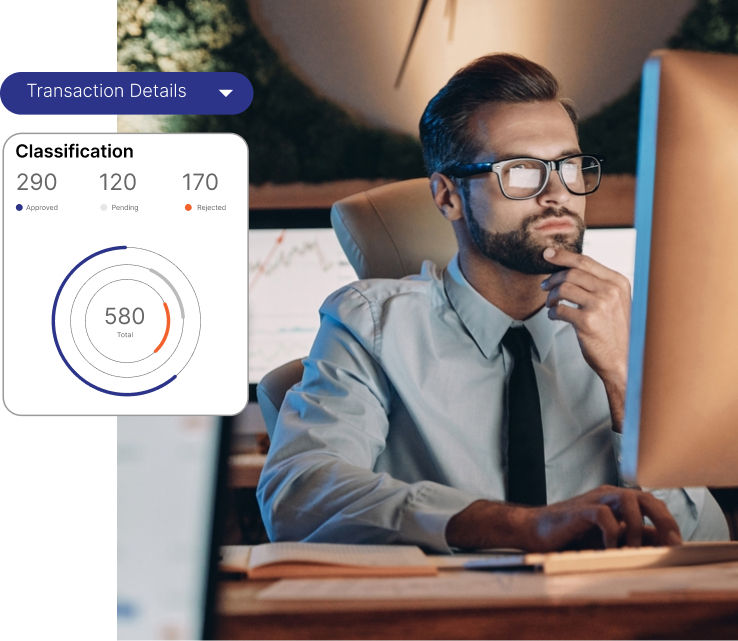

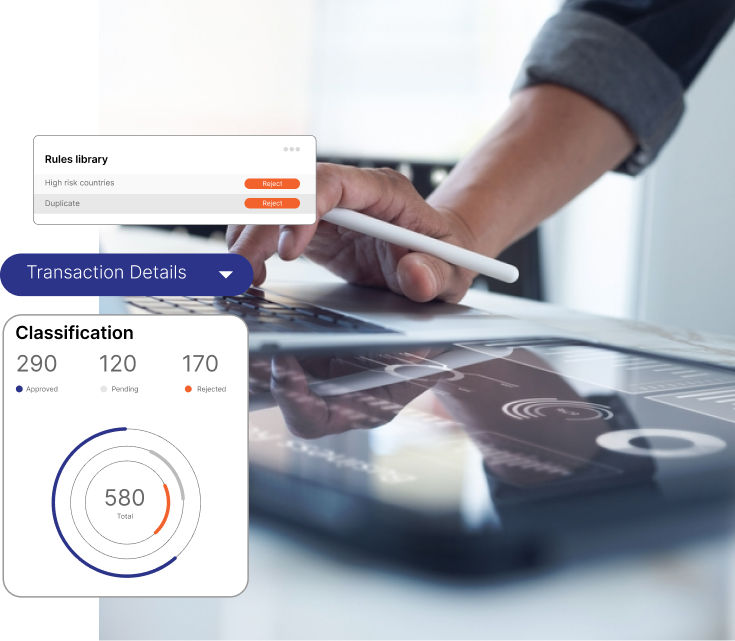

Full Compliance Across Jurisdictions

Centralise, simplify, and scale your compliance efforts across jurisdictions and regulators. Use regulator specific templates or create your own rules and workflows.

How does the KYC verification process work?

The KYC verification process follows a similar format of steps applicable to various industries, although the level of detail needed may vary based on customer risk profile and local laws.

Identity verification and document checks

The first step is to confirm who the customer is. This involves providing one or more government-issued photograph identification documents: passport, National Identity Card, or Driving License.

Advanced KYC solutions combine human intervention and automated tools to verify whether documents have been tampered with, expired, or are fake.

Biometric authentication features, such as facial recognition technology, to match against the photo on the ID document, are increasingly becoming part of effective KYC solutions.

Address verification and proof of address

You also need proof of address (POA) to confirm residency. These can be utility bills, bank statements, or official letters from government departments that are less than 3 months old.

When conducting online onboarding, address verification through database checks against voter lists, credit bureaus, post office lists, etc., can supplement address verification, especially when obtaining physical addresses is challenging remotely.

Risk screening

The first step is to check customers against global sanctions lists and identify Politically Exposed Persons (PEPs). This prevents ties to prohibited entities and triggers extra scrutiny for high-influence individuals.

Screening includes searching for negative news to identify involvement in financial crimes or ethics scandals. This flags potential risks that have not yet reached official government watchlists.

Related content: Customer risk rating and models

Ongoing customer monitoring and re-verification

Risk is dynamic, so screening is an ongoing process. KYC does not end with customer onboarding.

Ongoing monitoring involves tracking customer behavior over time, flagging suspicious transactional activity, and updating the risk profile as circumstances change.

If a customer is designated as a PEP or listed in sanctions, quick action must be taken. Regular checks (re-verification) are also required, especially for higher-risk customers whose circumstances are more likely to change.

What is the difference between AML and KYC?

AML (Anti-Money Laundering) refers to the broader regulatory framework used to detect and prevent financial crime. KYC is used to identify and verify customer identities.

While KYC and AML are often used interchangeably, they refer to different things.

AML acts like an umbrella providing various tools, including Transaction Monitoring, Sanctions Screening, Customer Due Diligence, Enhanced Due Diligence (EDD), and Suspicious Transactions Reports (SAR). KYC is one of the core processes within that framework.

KYC as the foundation of risk-based compliance

Most modern AML systems operate on a risk-based approach (RBA). This means you conduct thorough reviews of high-risk customers and limited reviews of low-risk customers. KYC makes this approach possible.

Without good identification procedures and Customer Due Diligence (CDD) when onboarding customers, we cannot determine their level of risk, leaving our entire compliance programme vulnerable to challenges.

What is the difference between KYC & KYB?

KYC deals with individual customers, verifying their personal details, address, and financial risk assessment.

KYB (Know Your Business) follows a similar approach for corporate clients, and it involves verifying the legal entity, its ownership structure, and the beneficial owners (UBOs) associated with it, typically individuals who control 25% or more of a company’s ownership or voting rights under AML transparency rules.

Although both are required by law in several countries, the procedures and required documents differ.

What are the KYC requirements across industries?

The KYC requirements are not uniform across all sectors. Although the fundamental principles remain the same, varying levels of detail and document requirements exist depending on the industry and country.

Customer identification and due diligence

Customer Due Diligence (CDD) forms the basis of all good KYC practices. It involves identifying your customers, verifying their identities, understanding the nature of your relationship with them, and monitoring them on an ongoing basis.

All regulated businesses, banks, financial technologies, law firms, estate agents, and accountants must have effective systems of CDD in place.

Enhanced due diligence (EDD) for high-risk customers

Enhanced Due Diligence (EDD) is applied where customers pose heightened risks.

This includes Politically Exposed Persons (PEPs), individuals from countries classified as high risk by the Financial Action Task Force (FATF), including those on its gray or black lists, and those operating in high-risk sectors.

EDD means providing additional information, obtaining more documentation, identifying the sources of their assets and funds, and enhancing our ability to monitor them. EDD is mandatory whenever there is a high level of risk.

Record-keeping and audit trail obligations

Regulatory authorities require all financial institutions to keep KYC data for at least 5 years after termination of any business relationship - sometimes longer.

This includes copies of the documents collected, details of the verification processes conducted, risk assessment reports, media reports suggesting any negative information, and screening reports of sanctions.

A good system of maintaining KYC-related information acts as a strong defense mechanism in case of any surveillance conducted by the regulators.

How do KYC requirements differ across industries?

KYC requirements vary depending on regulatory exposure.

Banks comply with the most stringent KYC rules worldwide and must follow detailed AML frameworks.

Fintech companies follow similar guidelines but leverage digital and automated systems to carry out their tasks.

Cryptocurrencies are now fully covered by KYC requirements as per the latest guidance on virtual assets issued by the Financial Action Task Force (FATF), including the Travel Rule applicable to transfers of cryptocurrency.

Non-Financial Companies, such as Lawyers, Estate Agents, and Accountants, have lesser yet strict KYC requirements under Anti Money Laundering (AML) laws in most jurisdictions.

Read also:

What are the methods to conduct KYC verification?

Tools available to conduct KYC have evolved rapidly. Most of the Compliance teams employ a combination of techniques to gather the required information about the customer.

Document-based verification

This is the most established method. A customer presents a physical or digital copy of their ID and proof of residence, which is then thoroughly reviewed - manually or via an automated software program for authenticity.

This method is very reliable. Nevertheless, it is rather slower than newer techniques and is increasingly supported by more dynamic verification methods in online onboarding environments.

Biometric and video KYC

Biometric verification makes use of facial recognition or fingerprint scanning to verify that the person showing their ID is really who they say they are.

Video KYC involves a compliance officer or an automated system checking identity during a real-time video session.

This method is legally recognized in markets like India and Germany, and also in several UAE-regulated sectors. It provides a human element to digital onboarding without the need to physically visit the premises.

azakaw's Biometric Verification

Use liveness tests to verify identities and prevent ID fraud. Distinguish legitimate users from fraudsters to safeguard your business.

Database and register checks

Automated checks run alongside document checks. These include sanctions lists such as OFAC, the United Nations, and the European Union, along with PEP databases, adverse media sources, and corporate registries.

These checks are essentially instantaneous. Moreover, they produce risk signals that a document alone would never reveal, such as links to ongoing financial crime investigations or very recent adverse media coverage.

Real-time identity verification with AI

Artificial intelligence and machine learning technology are behind virtually every contemporary KYC platform nowadays.

AI can read documents and extract information. It can then cross-check this data across numerous sources, detect fraud patterns, and flag anything unusual, all within just a couple of seconds.

This greatly reduces the need for manual reviews. Consequently, the compliance team can concentrate on very complex or high-risk cases that require human judgment.

azakaw's AI-Powered Solution

An AI platform that provides insights for enhanced reporting and cuts onboarding time from days to minutes, ensuring a seamless client experience.

What are the types of KYC Checks?

The actual type and depth of a KYC check will vary a lot because it all depends on who the customer is and the inherent level of risk they carry.

Every customer will have a different amount of attention focused on them - not all of them require the same level of investigation after all.

Individual KYC vs. Business KYC (KYB)

An individual KYC check will verify the identity, address, and risk profile of a natural person.

Business KYC or KYB checks the existence of a business entity: its registration details, its ownership structure, and the ultimate controllers owning 25 per cent or more.

Business KYC is more complex and will also be more time-consuming, but it is essential in all regulated markets if the customer is a corporate body rather than an individual person.

The End-to-End Platform

Looking for a solution that safeguards your business? Discover how azakaw is the perfect solution for you with digital KYC & KYB compliance modules.

Simplified vs. Enhanced due diligence

Simplified due diligence (SDD) can be used when the risk of money laundering is clear enough to be easily seen - low-value products or businesses with a well-known public listing, for example.

Standard CDD will cover the majority of customers themselves.

An EDD will be required when the risk is higher. The key thing to remember is that your risk-driven approach must be able to clearly explain why one level or another applies to every single customer, and the relevant regulators will certainly scrutinize your explanation.

What is eKYC?

eKYC means Electronic Know Your Customer, and it uses digital technology to complete the entire KYC process online. It is now a standard feature at most Fintech companies and is increasingly adopted by traditional banks operating in countries such as the UAE, Singapore, and the European Union.

How does eKYC work?

eKYC (electronic Know Your Customer) verifies customer identity digitally using automated document capture, biometric authentication, and real-time database checks.

Instead of submitting physical documents in person, customers upload identification documents online, which are validated using OCR technology, facial recognition, and sanctions screening systems.

Financial institutions use eKYC to confirm identity, assess risk levels, and meet AML compliance requirements during remote onboarding.

Unlike traditional KYC processes that rely on manual document review, eKYC platforms perform multiple verification checks simultaneously:

identity validation

proof-of-address confirmation

sanctions screening

adverse-media screening.

This allows organizations to complete customer onboarding faster while maintaining regulatory compliance standards.

Regulators such as the Monetary Authority of Singapore (MAS) and authorities in the United Arab Emirates support the use of digital identity verification frameworks that enable financial institutions to implement secure and compliant eKYC onboarding workflows.

99% Accuracy to Reduce Fraud Risk

Verify a range of identity documents, from passports and driving licences to national IDs. azakaw streamlines your process and eliminates the need to utilise multiple verification systems.

KYC challenges and solutions

Even strong KYC frameworks hit practical friction. Knowing where the problem areas are helps you build something more robust from the start.

Manual processes, delays, and high rates of false positives

Manual KYC processes are slow, taking several days or even weeks. They also lead to high rates of false positives, where genuine customers are incorrectly identified as posing financial risks, damaging the experience of opening an account with the bank, and leading to unnecessary extra work.

Automated KYC solutions help resolve these challenges, but adequate training of the software solution is necessary to avoid creating more problems than we solve. Excessive stringency in the automated threshold criteria can lead to new challenges.

Verify Business Identities

Simplify business verification and onboarding with our comprehensive KYB software. Identity and verify ultimate beneficial owners and directors, and evaluate corporate documents with our AI engine.

Balancing compliance and customer experience

There is a huge challenge in striking a good balance between robust KYC procedures and providing a smooth customer experience. Requesting too much information at the initial stage leads to drop-offs, sometimes significant ones.

The solution lies in implementing a risk-based approach: gather the necessary details based on the level of risk posed by the customer rather than relying on a generic checklist.

Effective digital onboarding tools provide easy avenues for collecting required documents without compromising on our high standards of compliance.

Technology integration

Increasingly effective KYC systems rely heavily on advanced technologies such as AI, automation, and Transaction Monitoring. Integrating KYC platforms with robust AML and transaction monitoring systems is easier said than done.

There are several challenges related to data silos, outdated technology infrastructure, and inconsistent data formats, resulting in regulatory blind spots.

Companies that succeed in achieving good technological integration invest in platforms that offer a single data layer for Customer due diligence, transaction monitoring, and case management capabilities.

What happens if a company fails to comply with KYC requirements?

Failure to comply with Know Your Customer (KYC) requirements can result in significant regulatory penalties, operational restrictions, reputational damage, and, in serious cases, criminal liability.

Financial institutions must verify customer identity as part of anti-money laundering (AML) compliance programs established by regulators such as the FCA, FinCEN, MAS, and authorities across the European Union.

Financial fines and enforcement actions

Financial penalties for poor AML/KYC controls amount to nine-figure values regularly.

Deutsche Bank, HSBC, and Goldman Sachs have been dealt heavy blows from enforcement actions in recent years. The USA's FinCen, the UK's FCA, and Singapore's Monetary Authority have imposed hefty penalties in various cases.

The trend towards increasing financial penalties and personal liability for top-level officials, rather than companies, continues.

Read also: Money laundering charges in the UAE

Operational and reputational consequences

Beyond financial penalties, non-compliance may result in license suspension, restrictions on business activities, and long-term reputational damage.

Regulatory investigations can limit an organization’s ability to operate in certain jurisdictions and weaken relationships with financial partners, investors, and counterparties.

Criminal liability risks

In cases involving serious or repeated compliance failures, regulators may initiate legal action against responsible individuals as well as institutions.

For example, the UK Financial Conduct Authority (FCA) can pursue criminal proceedings where failures contribute to financial crime through gross negligence or willful misconduct.

What regulations govern KYC requirements?

Know Your Customer (KYC) operates within a web of international and domestic laws and regulations.

Getting a clear understanding of the global and national KYC regulatory framework enables us to understand the AML/CFT expectations in our area of operations.

FATF recommendations and regional regulations

The Financial Action Task Force (FATF) sets the global standard for combating money laundering and terrorist financing through its 40 Recommendations.

These recommendations require countries to implement customer identification procedures, customer due diligence (CDD), enhanced due diligence (EDD), and ongoing monitoring as part of a risk-based compliance framework.

FATF also maintains lists of high-risk jurisdictions, commonly known as black-list and grey-list countries.

Customers connected to these jurisdictions typically require enhanced monitoring and additional verification steps under AML regulations.

Regional AML laws and regulatory authorities

Most national KYC requirements are derived from FATF standards but implemented through regional legislation and supervisory authorities.

Key regulatory frameworks include:

European Union Anti-Money Laundering Directives (AMLD)

United States Bank Secrecy Act (BSA)

UAE Federal Anti-Money Laundering Law

Monetary Authority of Singapore (MAS) AML/CFT notices

These frameworks define how regulated institutions must perform identity verification, maintain customer records, monitor transactions, and report suspicious activity.

Financial Intelligence Units (FIUs) also cooperate internationally, meaning weaknesses in KYC controls in one jurisdiction may trigger increased scrutiny across multiple markets.

Read more:

Frequently Asked Questions about KYC

Is KYC mandatory for all businesses?

Although not all businesses need to comply with KYC rules, a wide range of financially regulated industries have to conduct KYC activities.

Banks, Fintech, Crypto companies, Law Firms, Chartered Accountants, Real Estate Agents, and Designated Non-Financial Businesses and Professionals are required to adhere to KYC guidelines as per the FATF-compliant country's laws.

What documents are required for KYC?

Standard KYC requires a government-issued photo identification card: a passport, national ID card, or driver's license, and proof of address not older than 3 months, such as utility bills or bank statements.

Financial institutions dealing with a high level of risks shall provide information about their source of funds, corporate documents of ownership, and additional layers of verification through Biometric/ Video KYC.

When should KYC be updated?

There is no general rule, although most of the regulatory framework specifies periodical re-verification based on the level of risk. High-risk customers need to be verified annually. Medium-risk customers can be checked after 3-5 years.

How long does KYC verification take?

The time required to complete KYC verification depends on the method used and the customer’s risk level.

Traditional KYC processes that involve manual document checks may take several days. However, modern electronic KYC (eKYC) systems using automated document verification, biometric authentication, and database screening can complete identity checks within minutes.

Additional verification steps such as enhanced due diligence (EDD), sanctions screening, or source-of-funds checks may extend the timeline for higher-risk customers.

What happens if KYC verification fails?

If KYC verification fails, organizations are usually unable to establish or continue a business relationship with the customer. Financial institutions must confirm customer identity before onboarding to comply with anti-money laundering (AML) regulations.

When verification cannot be completed successfully, businesses may request additional documentation, apply enhanced due diligence measures, or decline the relationship altogether.

In regulated sectors such as banking, fintech, and cryptocurrency services, completing KYC checks is a legal requirement before providing services.

Conclusion

Know Your Customer (KYC) is a key area of compliance for any organization that is subject to regulation.

Good KYC practices help the organization to protect itself from money laundering and financial crimes, keep the regulators happy, and establish good levels of transparency needed by serious business partners to deal with us!

Whether you are conducting KYC checks for a Bank, Fintech, Cryptocurrency Exchange, or Professional Services Firm, the basics of all KYC systems are the same:

verify the identity of the customer

identify the level of risk associated with the customer

keep a close watch on the customer’s behavior over a period of time, maintaining comprehensive records.

The tools available to facilitate effective KYC measures are advanced, including eKYC, Biometric Authentication, Artificial Intelligence-driven Automation, etc.

However, having strong processes is essential! Creating a solid KYC foundation allows all other areas to fall into place.

Video overview of KYC

Related articles