Money Laundering Policy Template: Designing controls that survive real-world pressure

- azakaw

- Mar 18

- 9 min read

Updated: Jun 3

An Anti-Money Laundering (AML) policy is not just a regulatory requirement. It defines how financial crime risk is identified, escalated, and controlled across an institution.

Yet many AML policies fail in practice. Not because rules are missing, but because they cannot survive commercial pressure, fragmented systems, or overlapping regulatory expectations across jurisdictions.

This article explains what an AML policy should include, how global regulatory frameworks shape its structure, and how institutions can design a policy that works operationally, not just on paper. It also includes a practical AML Policy template to help teams structure and strengthen their own AML policies.

Money Laundering Policy - Key Takeaways |

|

|

|

|

|

|

|

|

|

|

|

What is an Anti-Money Laundering (AML) Policy?

An Anti-Money Laundering (AML) policy is a structured set of internal procedures, controls, and regulations that institutions use to prevent criminals from disguising illegally obtained funds as legitimate income.

It defines how an institution identifies, measures, and responds to Money Laundering risk. At its core, the AML policy governs how proceeds of crime are detected, investigated, and reported.

The AML Policy Statement sets the tone from the top. The policy itself translates that tone into operational decisions.

It determines when Customer Due Diligence (CDD) is sufficient, when Enhanced Due Diligence (EDD) is triggered, how Beneficial Ownership is verified, and how far the institution will go to identify the Ultimate Beneficial Owner (UBO) when structures are complex or opaque.

The AML policy is not separate from the AML Governance Framework. It is the governance framework expressed in executable terms.

A weak policy produces ambiguity. Ambiguity produces inconsistent decisions. Inconsistent decisions produce regulatory exposure.

TIP: Read our guide about money laundering prevention

Why it matters for businesses and financial institutions

Institutions rarely fail because they lack data. They fail because they cannot convert data into defensible decisions under time pressure.

Transaction Monitoring systems generate alerts. Screening Procedures flag Politically Exposed Persons (PEPs) and sanctions matches. Without a coherent policy, those signals accumulate without resolution.

A robust money laundering policy reduces interpretive drift. It constrains discretion in onboarding, Ongoing Monitoring, and internal escalation.

It also defines the acceptable level of false positives. That is rarely acknowledged openly, yet every system embeds a tolerance threshold. Too low, and the risk passes through. Too high, and operations stall.

Who is required to have an AML Policy?

Entities required to have an AML policy include financial institutions (banks, credit unions), money service businesses (MSBs), crypto exchanges, law firms, casinos, real estate agents, and high-value dealers.

Generally, any business handling large cash transactions or deemed "high-risk" for money laundering must adopt, document, and implement these policies.

How often should the AML Policy be reviewed or updated?

The policy should move when risk moves, not when governance calendars allow it.

Formal cycles exist, usually annual. They are insufficient. Policy drift occurs faster than regulatory updates.

Changes in typologies, product offerings, or geographic exposure require interim adjustments.

An AML Risk Assessment that is updated annually but feeds a static policy is a known failure mode.

What are the key components of an AML Policy?

The key elements of an AML policy are: risk assessment, CDD and KYC, transaction monitoring and reporting, record keeping, employee training, and a compliance Officer.

Risk assessment procedures

An AML Risk Assessment defines how the institution perceives its exposure. Most frameworks claim a Risk-Based Approach.

In practice, many assessments are reverse-engineered from existing controls. That produces circular logic. High-risk classifications are assigned where controls already exist, not where risk is genuinely concentrated.

Effective risk assessment separates inherent risk from control effectiveness. It recognises that product complexity, jurisdictional exposure, and client type interact.

It also accepts that some risks cannot be mitigated economically. Those exposures should be explicitly accepted or exited, not disguised within scoring models.

AI-driven risk assessments

Gain comprehensive insights into a client’s investment risk appetite. Customise the risk assessment based on our templates or develop your own unique methodology.

Customer Due Diligence (CDD) and Know Your Customer (KYC)

Customer Due Diligence (CDD) and Know Your Customer (KYC) processes are often treated as onboarding formalities. They are, in fact, the foundation of every downstream control.

Weak onboarding contaminates Transaction Monitoring, Sanctions Screening, and UBO identification.

Enhanced Due Diligence (EDD) is where policies become operationally uncomfortable. Politically Exposed Persons (PEPs), complex ownership structures, and high-risk jurisdictions require deeper investigation.

The policy must define how far the institution is willing to go. There is no universal standard for verifying Beneficial Ownership in layered structures. Institutions choose thresholds. Those thresholds determine exposure.

Onboard global customers with ease

Create customised onboarding flows and verify individual customers or legal entities with ease while ensuring full AML compliance. Minimise manual intervention and reduce errors with azakaw.

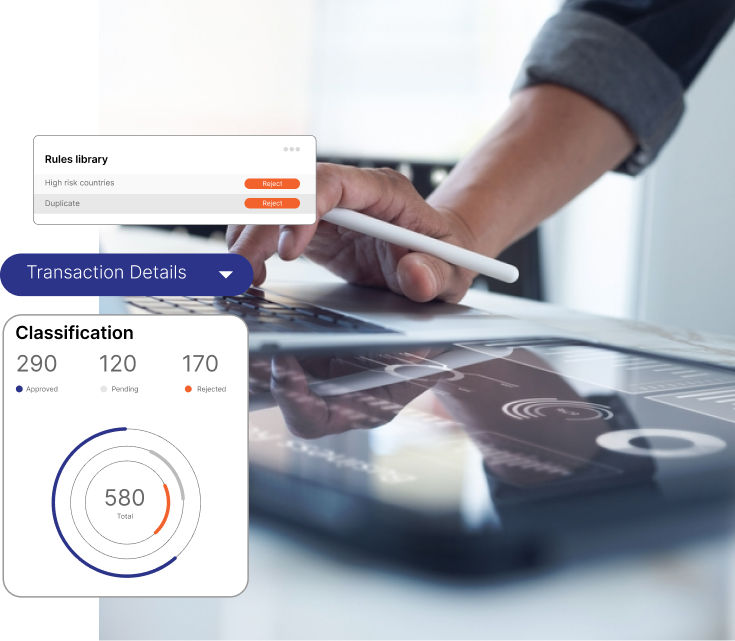

Transaction Monitoring and Reporting

Transaction Monitoring systems do not detect Money Laundering. They detect deviations from expected behaviour. The policy determines what constitutes expected behaviour. That baseline is often poorly defined.

Suspicious Activity Report (SAR) and Suspicious Transaction Report (STR) processes are shaped by Reporting Obligations to the Financial Intelligence Unit (FIU).

The decision to file is rarely clear-cut. Policies that rely on generic “suspicion” criteria push decision-making onto analysts without sufficient guidance.

Over-reporting creates noise. Under-reporting creates liability. The balance is not stable across jurisdictions.

Stay ahead of risk with azakaw

Learn how azakaw, an end-to-end compliance platform powered by AI, detects, prevents, and resolves suspicious activities in real-time. Safeguard your business!

Record-Keeping requirements

Record-keeping requirements are often reduced to retention periods. That misses the point. The value lies in reconstructability.

An Audit Trail must allow a regulator to understand why a decision was made at a specific moment, based on information available at that time. Systems that store AML data but cannot reconstruct the decision context fail under scrutiny.

Confidentiality obligations intersect with record keeping. Internal access must be controlled without impairing investigations. Poorly designed access controls either expose sensitive data or obstruct legitimate analysis.

Employee training programs

An AML employee training program is only effective if it reflects actual decision points. Generic AML training does not improve judgment.

Analysts need exposure to real red flags of money laundering, including ambiguous cases. Training that avoids uncertainty produces compliance that collapses under pressure.

Whistleblower Policy integration matters. Internal reporting of concerns must be credible. If employees believe escalation carries risk without protection, issues remain buried until external intervention.

Compliance officer

The AML Officer or Compliance Officer's responsibilities extend beyond oversight. The role mediates between commercial objectives and regulatory expectations.

If the AML Officer is structurally subordinate to revenue functions, escalation authority becomes symbolic.

The Independent Audit Function must test not only control existence but also control effectiveness. Many audits confirm that procedures are followed. Fewer tests whether those procedures detect actual risk.

How to create a money laundering policy template

Step-by-Step Guide

An AML Policy Template is often built by adapting regulatory language. That approach produces documents that satisfy form but not function.

A workable template starts from decision points. It identifies where staff must act under uncertainty, then defines acceptable actions.

To create an effective AML policy template:

Start by defining onboarding procedures: Specify what constitutes sufficient KYC and when onboarding must be refused.

Define CDD and EDD triggers: Clarify when standard due diligence is sufficient and when enhanced checks become mandatory.

Establish sanctions screening rules: Set match thresholds, escalation paths, and resolution timelines for screening alerts.

Clarify beneficial ownership verification requirements: Define how Ultimate Beneficial Owners (UBOs) must be identified, especially in complex structures.

Document internal reporting procedures: Explain how suspicions move from front-line staff to the AML Officer or MLRO.

Define external reporting obligations: Specify when Suspicious Activity Reports (SARs) must be submitted to regulators.

Set escalation thresholds and decision authority levels: Identify when cases move from operational teams to compliance leadership.

Integrate all procedures into a single compliance manual: Avoid fragmented documentation that creates responsibility gaps and regulatory exposure.

Adapting the template to your organization

Templates fail when they ignore operational constraints. A high-frequency payments institution cannot apply the same Transaction Monitoring thresholds as a private bank without overwhelming its systems.

Our experience allows us to say that adaptation requires alignment with transaction volume, product complexity, and staffing capacity.

Global institutions face additional tension. OFAC requirements may conflict with EU data protection constraints. MAS AML Guidelines may impose expectations that differ from DFSA or ADGM frameworks.

The policy must explicitly resolve these conflicts. Silence is not neutrality. It is exposure.

The End-to-End Compliance Tool

With azakaw you can use regulator-specific templates or create your own rules and workflows according to your business needs.

Common mistakes to avoid

Policies often assume that controls operate as designed. They rarely account for system latency, data quality issues, or manual overrides.

Another common failure is excessive reliance on automated scoring without understanding model limitations.

There is also a tendency to overcomplicate language. Ambiguous phrasing increases discretion at the point of execution. Precision reduces debate but requires institutional commitment.

Many organisations avoid that commitment because it restricts flexibility in commercial negotiations.

Free Money Laundering Policy Template

The Money laundering policy template provided here is not a narrative policy document. It is the operational layer that sits behind the policy. It translates policy statements into structured decision points across onboarding, due diligence, monitoring, escalation, and reporting.

Rather than defining principles, it enforces how those principles are applied in practice.

It standardises inputs, reduces discretion where it creates risk, and ensures that key actions, such as Customer Due Diligence (CDD), Transaction Monitoring, Sanctions Screening, and Suspicious Activity reporting, are documented in a way that can withstand audit and regulatory scrutiny.

The template is available in both Excel and Word formats and includes jurisdiction-specific structures for the United States, United Kingdom, United Arab Emirates, and Singapore.

The Excel version is designed for operational use, enabling consistent data capture and control execution through structured inputs.

The Word version complements it by providing a clear, auditable format suitable for documentation, internal alignment, and regulatory review.

Each reflects differences in regulatory focus, including reporting expectations, beneficial ownership requirements, escalation models, and monitoring obligations.

It should not be used as a standalone policy. It is designed to work alongside a formal AML Policy and Compliance Manual, acting as the execution layer that ensures those documents are consistently applied.

The value of the template lies in reducing variability in decision-making and making control application visible, testable, and defensible.

Tailoring the policy to operational reality

A Money Laundering Policy that mirrors regulatory text but ignores business model specifics creates blind spots. Tailoring is not optional. It determines whether controls are applied where risk actually materialises.

The benefits of a money laundering policy template

An AML Policy Template accelerates implementation but also standardises decision logic. That reduces variability across teams and jurisdictions. It also enables faster onboarding of staff into the AML Compliance Program.

There is a trade-off. Standardisation can suppress local insight. Analysts may follow template-driven decisions even when contextual factors suggest escalation.

Templates improve consistency at the cost of sensitivity. Institutions need to decide which failure mode they prefer.

Legal and regulatory framework

Regulatory frameworks define minimum expectations. 6AMLD expands criminal liability and practices.

The Financial Action Task Force (FATF) sets the baseline through its FATF Recommendations. These are interpreted differently across jurisdictions. Institutions operating globally must navigate inconsistent implementation.

Jurisdiction-specific guidelines

FinCEN and OFAC impose stringent reporting and sanctions regimes in the US.

The UAE Central Bank AML Guidelines reflect a rapidly evolving supervisory environment.

MAS AML Guidelines emphasise risk management discipline.

DFSA and ADGM frameworks introduce their own supervisory expectations.

Alignment across these regimes is rarely complete.

FAQs about AML Policy

What are the penalties for non-compliance?

Penalties extend beyond fines. Regulatory action can restrict business operations, impose remediation programs, and trigger reputational damage that affects counterparties. In some jurisdictions, senior management faces personal liability under 6AMLD.

What are the indicators of money laundering?

Red Flags of Money Laundering include unusual transaction patterns, inconsistent client behaviour, and complex ownership structures without a clear economic rationale. Indicators are context-dependent. A pattern that is suspicious in one business model may be normal in another.

What is the policy statement on money laundering?

The AML Policy Statement defines the institution’s stance on Money Laundering risk, its commitment to compliance, and the authority of the AML Officer. It sets expectations for adherence to Internal Controls, Reporting Obligations, and Confidentiality Obligations.

Conclusion

A Money Laundering Policy is often treated as a control document that stabilises risk. In practice, it redistributes risk. Tightening controls shifts pressure onto onboarding and client retention.

Relaxing thresholds reduces operational friction but increases exposure to regulatory action. The policy becomes a negotiation between compliance and commercial imperatives.

The unresolved issue is not technical. It is institutional. As Transaction Monitoring becomes more automated and Screening Procedures more sophisticated, the remaining risk concentrates in judgment calls that cannot be standardised.

Institutions continue to invest in systems that promise detection while leaving the hardest decisions to individuals operating within policies that still avoid defining how much uncertainty they are prepared to tolerate.

Related articles