AML risk management: what it is and how it shields your business

- azakaw

- Mar 26

- 14 min read

Updated: Apr 30

AML risk management is the operational layer of anti-money laundering compliance that determines how institutions monitor exposure, apply controls, and respond to suspicious activity in practice.

For banks, fintechs, crypto firms, and other regulated businesses, effective AML risk management is essential not only to meet supervisory expectations but also to maintain control effectiveness, protect reputation, and support consistent onboarding and monitoring decisions.

This guide explains how AML risk management works in practice, what regulators expect from it, and how organisations can build frameworks that remain defensible under regulatory scrutiny.

Risk management key takeaways |

|

|

|

|

|

|

|

|

What is AML risk management?

AML risk management is the process through which financial institutions monitor, control, and mitigate money laundering risk on an ongoing basis. It translates AML risk assessment findings into operational controls such as Customer Due Diligence (CDD), transaction monitoring, escalation decisions, and Suspicious Activity Report (SAR) filing.

AML risk assessment defines exposure. AML risk management determines how institutions respond to that exposure in practice through controls, escalation decisions, and ongoing monitoring.

AML risk management is not a policy construct. It is a system of operational decisions taken under regulatory pressure, where imperfect information meets irreversible consequences.

The term “what is AML risk management” is often answered with frameworks and definitions, but in practice, AML risk management resolves into one question:

how an institution decides which risks it will carry and which it will actively suppress, knowing that both choices create exposure.

What is the difference between AML risk management and AML risk assessment?

In short, AML risk assessment defines risk exposure. AML risk management determines how that exposure is controlled in daily operations.

Let's go into the details. The difference between AML risk assessment and risk management is operational rather than conceptual:

AML risk assessment produces a static view. It categorises inherent and residual risk across customers, products, and jurisdictions. It is periodic, structured, and often well documented.

AML risk management absorbs that assessment and then has to function in motion. It determines how Customer Due Diligence (CDD) is applied in edge cases, how Enhanced Due Diligence (EDD) is triggered when data is incomplete, and how transaction monitoring controls behave when volumes spike or patterns shift. The AML risk management process is where institutions either maintain discipline or quietly erode it through exceptions, overrides, and tolerance drift.

In practice, assessment without management creates a false sense of control. Management without a credible assessment produces inconsistency that regulators detect quickly.

What are the objectives of AML compliance risk management?

AML compliance risk management aims to:

Maintain control effectiveness under operational pressure

Ensure consistent application of CDD and EDD

Preserve escalation integrity

Support defensible SAR decisioning

Align monitoring intensity with risk appetite

The stated objectives of AML compliance risk management include detection, prevention, and reporting. Those are baseline expectations.

The real objective is to maintain control effectiveness under operational strain. That includes ensuring that AML policies and procedures are actually followed when timelines compress, that ongoing monitoring of AML processes do not degrade under volume, and that escalation pathways remain intact when commercial pressure increases.

Senior management oversight and board-level accountability exist because these objectives conflict with revenue and client retention.

The system is designed to force visibility of that conflict, not to remove it.

Benefits of AML risk management for regulated businesses

AML risk management helps regulated businesses meet supervisory expectations, reduce financial and legal exposure, apply proportionate customer onboarding controls, and maintain consistent monitoring and governance across their operations.

Together, these benefits help institutions operate more securely, maintain stronger regulatory credibility, protect their reputation, and deliver a more consistent and trustworthy customer experience across their services.

Meeting regulatory expectations across global AML frameworks

Regulators do not expect institutions to eliminate money laundering risk. They expect them to demonstrate that risk is understood, documented, and consistently controlled.

Authorities such as the Financial Crimes Enforcement Network, Financial Conduct Authority, and Basel Committee on Banking Supervision assess whether AML controls behave coherently across cases and remain aligned with a documented Risk-Based Approach.

Frameworks established by the Financial Action Task Force, the European Union Anti-Money Laundering Directives (AMLD), and the Bank Secrecy Act (BSA) do not prescribe outcomes; they require defensibility.

Recommendation 1 of the Financial Action Task Force establishes the expectation that institutions implement a documented Risk-Based Approach supported by ongoing monitoring and control effectiveness testing.

According to our experience, institutions must be able to explain how risk decisions were made, how controls were applied, and how monitoring supports those decisions over time.

Supervisors increasingly focus on control effectiveness, audit trail integrity, and SAR decision consistency rather than isolated incidents, reinforcing the importance of structured AML risk management frameworks across jurisdictions.

Cooperation between Financial Intelligence Units through the Egmont Group reinforces expectations that weaknesses in AML risk management frameworks will be visible across jurisdictions.

Reducing financial, legal, and reputational exposure

Financial penalties are visible but rarely the most damaging outcome. Remediation costs, independent monitorships, and system rebuilds consume resources over multiple years.

Legal exposure extends beyond fines into restrictions on business activity. Reputational damage affects correspondent banking relationships and access to liquidity.

These risks are not evenly distributed. Banking AML risk management faces different pressure points compared to fintech AML risk management or crypto AML risk management.

Payment service providers (PSPs) and fintechs often underestimate how quickly regulators escalate expectations once transaction volumes reach systemic relevance.

Supporting more effective and proportionate customer onboarding

AML risk management improves customer onboarding by ensuring Customer Due Diligence (CDD) and Enhanced Due Diligence (EDD) requirements are applied proportionately to risk exposure rather than uniformly across all customers.

This allows institutions to reduce unnecessary onboarding friction for lower-risk customers while maintaining enhanced scrutiny where exposure is higher.

As a result, onboarding decisions become more consistent and easier to justify during supervisory reviews.

Improve User Digital Onboarding

Transform end-to-end onboarding with customised flows tailored to your business needs using our secure solution.

Improving monitoring consistency and control effectiveness

Risk management frameworks help ensure that transaction-monitoring controls, sanctions screening, and customer risk scoring remain aligned with behavioural patterns, geographic exposure, and product risk rather than static assumptions.

Continuous recalibration reduces the likelihood that monitoring scenarios become misaligned with exposure over time and supports consistency between monitoring outputs and Suspicious Activity Report decision-making expectations.

Strengthening governance transparency and decision accountability

AML governance is not an overlay. It is embedded in decision-making authority.

Compliance governance determines whether risk acceptance decisions are transparent or implicit.

Internal controls, control effectiveness testing, and escalation structures define whether issues are contained or propagated.

Institutions that treat the AML compliance framework design as a compliance exercise rather than a governance mechanism create blind spots that only surface during enforcement.

How AML risk management works

AML risk management works as a continuous operational cycle that identifies risk, applies controls such as CDD and transaction monitoring, escalates suspicious activity through investigation and SAR decisioning, and recalibrates risk scoring based on ongoing monitoring and regulatory expectations.

Overview of the AML risk management lifecycle

In theory, the AML risk management lifecycle follows this approach:

Identify risk

Assess risk levels

Implement controls

Ongoing monitoring

Suspicious activity escalation

Recalibration of risk scoring

However, how AML risk management works in practice is not linear. The lifecycle described in policy documents is a simplification.

Risk identification, assessment, control design, and monitoring occur simultaneously across different layers of the institution.

The difference between theory and practice emerges quickly. Customer risk, product and service risk, geographic risk, and delivery channel risk do not arrive neatly classified.

They surface through onboarding friction, transaction monitoring alerts, and escalation failures.

AML compliance management is therefore not about eliminating risk. It is about structuring exposure in a way that can be justified under scrutiny.

Customer onboarding triggers CDD and EDD. Transactions trigger monitoring and alerts. Alerts trigger investigation and potential Suspicious Activity Reports (SARs).

Each stage feeds back into dynamic risk scoring and control recalibration.

The AML risk management lifecycle is therefore recursive, not sequential.

From risk identification to risk mitigation

Money laundering risk management depends on translating abstract risk categories into actionable controls.

Risk identification defines exposure. AML risk mitigation determines how aggressively controls are applied.

Risk mitigation measures include adjusting transaction monitoring thresholds, increasing EDD requirements for certain geographies, and restricting product features.

Each decision carries a cost. Tight controls increase false positives and customer friction. Loose controls increase regulatory exposure.

The trade-off is unavoidable. Institutions that claim otherwise are not measuring their systems accurately.

Continuous monitoring and review

Ongoing monitoring is where most frameworks fail. Controls are implemented correctly at launch and then degrade.

Transaction monitoring models become outdated. Customer profiles are not refreshed. Escalation thresholds drift.

Regulators focus heavily on ongoing monitoring of AML because it reveals whether an institution is managing risk or simply documenting it.

Continuous review is not periodic reporting. It requires active recalibration of controls based on emerging patterns, including typologies identified by UNODC and national FIUs.

What are the key components of an AML risk management framework?

The main components of an AML risk management framework are Risk-Based Approach, clear policies and procedures, strong internal controls, and continuous monitoring to ensure that money laundering risks are identified, prioritised, and managed consistently across the institution.

Risk-based approach (RBA)

The Risk-Based Approach (RBA) is often treated as a principle. In practice, it is a constraint. Institutions cannot apply uniform controls across all customers and transactions. The RBA forces prioritisation.

That prioritisation is not neutral. It reflects business strategy. High-risk customers can be profitable. The decision to onboard them under EDD rather than reject them is a risk acceptance decision that must be documented and defensible.

Policies and procedures

AML policies and procedures define expected behaviour. They rarely capture actual behaviour. The gap between the two is where regulators focus.

Effective policies translate regulatory requirements into operational steps that can be executed under time pressure. Overly complex procedures create informal workarounds that undermine AML internal controls.

TIP: Get your Free Anti-Money Laundering Policy Template

Internal controls and governance

Internal controls determine whether policies are followed. Control effectiveness depends on design and execution.

Weak controls are often the result of conflicting incentives rather than poor documentation.

AML governance structures must ensure that escalation decisions are not overridden without documentation. Board-level accountability exists because these overrides often occur at senior levels.

Ongoing monitoring and escalation

Ongoing monitoring and escalation processes determine whether risks are contained or ignored. Automated alerts without effective investigation processes create noise rather than control.

Escalation must be timely and supported by clear decision frameworks. Delayed SARs filings are a common failure point and are closely scrutinised by regulators.

AML risk management controls and mitigation measures

AML risk management controls and mitigation measures translate risk assessments into operational safeguards, including customer due diligence, transaction monitoring, sanctions screening, and escalation procedures that ensure suspicious activity is identified, investigated, and reported consistently.

Customer due diligence and enhanced due diligence

Customer Due Diligence (CDD) and Enhanced Due Diligence (EDD) are often described as front-end controls.

In reality, they are continuous processes. Customer profiles evolve. Beneficial ownership structures change.

EDD is frequently applied inconsistently. High-risk customers are onboarded with enhanced scrutiny and then monitored using standard controls. This disconnect undermines the initial risk assessment.

Related content: Enhanced Due Diligence (EDD) meaning

Transaction monitoring controls

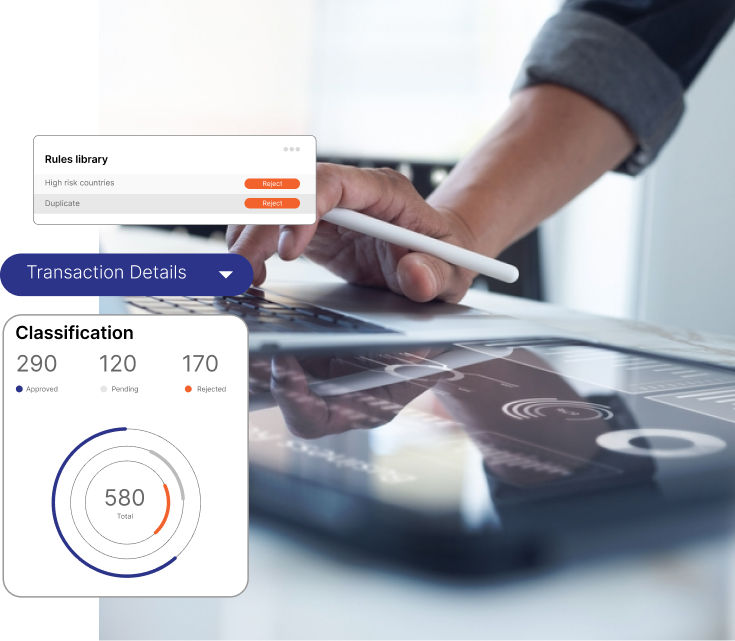

Transaction monitoring is the core of AML risk management controls. It is also the most fragile component. Models rely on historical patterns that may not reflect current behaviour.

Transaction monitoring controls generate alerts that must be triaged. High false positive rates create alert fatigue. Analysts begin to prioritise efficiency over thoroughness. This is where control effectiveness degrades.

Smart Transaction Monitoring System

Stay ahead of risks by detecting, preventing, and resolving suspicious activities in real-time with azakaw’s AI-powered AML solution. Learn how azakaw will change and safeguard your business!

Sanctions and PEP screening

Sanctions and Politically Exposed Persons (PEP) screening are highly sensitive areas. False negatives create immediate regulatory exposure. False positives create operational friction.

Screening systems must balance accuracy with usability. Overly broad matching criteria increase noise. Narrow criteria increase the risk of missed matches.

Internal reporting and escalation processes

Internal reporting and escalation processes connect operational controls to regulatory obligations. Suspicious Activity Reports (SARs) must be filed within defined timeframes and supported by a clear rationale.

Breakdowns in escalation often occur when responsibility is unclear. AML compliance management requires clear ownership of decision points.

What happens when AML risk management fails

When AML risk management fails, institutions typically face regulatory enforcement, financial penalties, reputational damage, and increasing accountability at the senior management level.

These consequences rarely arise from isolated incidents and usually reflect systemic weaknesses in internal controls and governance.

Regulatory enforcement actions and fines

Regulatory enforcement is rarely triggered by a single failure. It is triggered by patterns. Weak AML internal controls, poor audit trail, and inconsistent SARs decisioning signal systemic issues.

Fines are accompanied by remediation requirements that often exceed the cost of the penalty itself.

Control failures and ongoing exposure

Control failures rarely remain isolated. Once controls are bypassed or degraded, exposure accumulates. Institutions often discover issues during audits that have been present for extended periods.

Ongoing exposure is more damaging than isolated incidents because it indicates that the AML compliance framework design is not functioning as intended.

Reputational damage and loss of business

Reputational damage affects relationships with counterparties. Correspondent banks reassess exposure. Clients reconsider trust.

Loss of business often follows enforcement actions, particularly in cross-border contexts.

Personal accountability of senior management

Senior management and board members are increasingly held accountable. Regulatory focus has shifted toward individual responsibility.

Decisions that were previously considered operational are now examined at the governance level.

The role of financial institutions in AML risk management

Responsibilities of banks and financial institutions

AML risk management for banks involves systemic exposure. Banks operate as intermediaries in large transaction networks. Their controls affect broader financial stability.

Banking AML risk management requires robust transaction monitoring, effective CDD, and strong governance structures.

Read also: AML compliance for banks

Effortless Bank compliance software

Customise your onboarding processes and verify customers in an instant, ensuring a smooth and secure experience while meeting all compliance requirements effortlessly.

AML risk management in fintechs and payment providers

AML risk management for fintechs and PSPs is often underestimated. Rapid scaling introduces risk before controls mature.

Fintech AML risk management must address high transaction volumes, limited historical data, and evolving regulatory expectations.

Related content: AML Compliance for fintechs

Crypto AML risk management adds further complexity. VASPs operate in environments where transaction transparency does not eliminate anonymity.

azakaw for Fintech's AML Compliance

Simplify regulatory adherence and reduce operational costs with an all-in-one compliance platform that helps fintech companies stay ahead of evolving regulations.

Senior management and board oversight

Senior management oversight ensures that AML risk management is integrated into business decisions. Board-level accountability ensures that risk acceptance decisions are visible.

Without this oversight, AML compliance management becomes reactive.

AML compliance risk management across different risk areas

AML risk management operates across multiple risk dimensions, including customer risk, product and service risk, geographic exposure, and delivery channel risk, ensuring that monitoring intensity and control effectiveness remain aligned with actual institutional exposure.

Customer risk management

Customer risk is not static. It evolves with behaviour. Ongoing monitoring must reflect this.

Dynamic risk scoring systems attempt to capture these changes. Their effectiveness depends on data quality and model calibration.

Product and service risk management

Products and services create specific risk profiles. High-value transactions, cross-border payments, and anonymity features increase exposure.

Controls must be tailored to these characteristics.

Geographic risk management

Geographic risk is influenced by regulatory environments, enforcement intensity, and economic factors.

The UAE illustrates how rapidly this can change. Institutions must update geographic risk assessments frequently. Static classifications create blind spots.

Delivery channel risk management

Delivery channels affect visibility. Digital channels reduce friction but increase anonymity. Physical channels provide more control but are less scalable.

Risk management must adapt to these differences.

AML risk management and regulatory expectations

Regulatory expectations and enforcement focus

Regulators do not look for perfection. They look for patterns of unmanaged risk.

The Financial Crimes Enforcement Network (FinCEN), the Financial Conduct Authority (FCA), the Basel Committee on Banking Supervision (BCBS), and equivalent bodies assess whether institutions understand their exposure and whether controls behave consistently across cases.

AML compliance risk management exists to ensure that when a Financial Intelligence Unit (FIU), regulator, or auditor inspects a decision, the institution can demonstrate a coherent Risk-Based Approach (RBA) supported by audit trail, internal controls, and governance discipline.

Enforcement has shifted toward control failure rather than isolated incidents. Institutions are penalised for weak transaction-monitoring controls, ineffective SARs decision-making, and a poor audit trail, even when the underlying suspicious activity is ambiguous.

The Egmont Group’s emphasis on FIU cooperation reinforces this. Once a pattern is identified, cross-border exposure is no longer contained.

Global regulatory framework expectations

Anti-Money Laundering (AML) obligations anchored in the Financial Action Task Force (FATF), European Union Anti-Money Laundering Directives (AMLD), the Bank Secrecy Act (BSA), and parallel regimes do not prescribe outcomes. They prescribe defensibility.

Recommendation 1 of the Financial Action Task Force (FATF) establishes the global expectation that institutions implement a documented Risk-Based Approach supported by ongoing monitoring and control effectiveness testing.

Key insight: Institutions operating globally must reconcile these differences within a single AML risk management framework.

National regulators and supervisory authorities

National regulators translate FATF expectations into supervisory practice.

Authorities such as the Financial Conduct Authority (FCA), Financial Crimes Enforcement Network (FinCEN), and European supervisory bodies apply these standards through jurisdiction-specific examination priorities and enforcement approaches.

We always present as an example the UAE’s regulatory approach, which demonstrates increasing alignment with global standards while maintaining jurisdiction-specific requirements.

Regulatory examinations and audits

Regulatory examinations focus on control effectiveness. Audits assess whether policies are implemented consistently.

Documentation is critical. Decisions must be traceable through an audit trail.

UAE as an example of evolving supervisory pressure

The United Arab Emirates provides a clear example of this shift.

Historically viewed as a high-risk jurisdiction due to geographic risk and complex ownership structures, the UAE has moved aggressively to align with FATF expectations.

The creation of the Executive Office of Anti-Money Laundering and Counter Terrorism Financing, increased reporting obligations to the UAE FIU, and targeted enforcement against real estate and Virtual Asset Service Providers (VASPs) have changed the operating environment.

Institutions that treat UAE exposure as static high risk miss the point.

The regulatory environment is evolving faster than many internal AML risk management frameworks can adapt.

How technology supports AML risk management

AML compliance software supports risk management by aligning transaction monitoring, case management, and regulatory reporting within a single audit-ready environment.

AML compliance software and automation

AML compliance software is often presented as a solution. It is an enabler. Automation standardises processes and reduces manual error.

Poorly configured systems replicate existing weaknesses at scale.

Where AML compliance software is fragmented, control effectiveness becomes difficult to evidence.

Integrated environments, such as those offered by azakaw, which position their platforms as combining real-time transaction monitoring, case management, and reporting capabilities, can reduce this exposure by aligning automated alerts with documented investigative outcomes and a coherent audit trail.

The End-to-End Compliance Platform

Streamline compliance from identity and business verification to corporate compliance and AML transaction monitoring and risk management, reducing costs and complexity.

Real-time transaction monitoring

Real-time transaction monitoring allows institutions to detect suspicious activity as it occurs. This reduces response time.

It also increases alert volumes. Without effective triage, real-time systems can overwhelm analysts.

Dynamic risk scoring and alerts

Dynamic risk scoring uses data analytics, artificial intelligence (AI), and machine learning to adjust risk profiles.

These systems are not neutral. They reflect the data they are trained on. Bias and data gaps affect outcomes.

Automated alerts must be interpreted within context. Over-reliance on automation reduces critical analysis.

Scale Your Business with Confidence

Learn how the AI-powered azakaw solution enhances risk scores dynamically by analysing behavioural patterns, ensuring accurate identification of subjective elements.

Common AML risk management challenges

Common AML risk management challenges include:

false positives and alert fatigue

outdated monitoring models

governance delays

inconsistent escalation decisions

Managing false positives and alert fatigue

False positives consume resources. Analysts become desensitised. Important signals are missed.

Reducing false positives without increasing false negatives is technically difficult and operationally sensitive.

Keeping controls aligned with evolving risks

Risks evolve faster than controls. Emerging typologies identified by UNODC and FIUs require rapid adaptation.

Institutions often lag due to system limitations and governance processes.

Balancing compliance and customer experience

Strict controls create friction. Customers experience delays and additional requirements.

Relaxed controls increase exposure. The balance is not stable.

AML risk management best practices

Effective AML risk management frameworks typically:

Align monitoring intensity with risk appetite

Test control effectiveness regularly

Maintain escalation discipline

Integrate compliance governance with business decisions

Test the framework with independent reviews

Train staff

Frequently asked questions about AML risk management

Is AML risk management mandatory?

Yes. AML risk management is mandatory under global regulatory frameworks, including FATF recommendations, AMLD, and BSA. The requirement is not limited to implementation. It extends to demonstrating effectiveness.

Who is responsible for AML risk management?

Responsibility is distributed across operational teams, compliance functions, and senior management. Ultimate accountability rests with the board.

How often should AML risk management frameworks be reviewed?

Frameworks should be reviewed continuously. Formal reviews occur periodically. Ongoing monitoring provides real-time feedback.

Conclusion

AML risk management does not fail because institutions lack frameworks. It fails because decisions made under pressure are not consistent with those frameworks, and because technology amplifies both discipline and weakness without distinction.

The unresolved issue is not whether controls can be improved. It is whether institutions are willing to constrain profitable activity when dynamic risk scoring, real-time transaction monitoring, and regulatory expectations converge on the same point and leave no defensible space between commercial intent and enforcement exposure.

Related articles: