Best real estate compliance software in 2026: ranked & tested

- azakaw

- Apr 1

- 15 min read

Real estate brokers in the UAE and Saudi Arabia are now a named AML target, not a grey area. Most brokerages still verify buyers with one tool, screen manually or not at all, and have no answer when a regulator asks for a risk assessment.

This guide ranks the 10 best real estate compliance software options in 2026, GCC requirements first, international options after.

Quick comparison: best compliance software for real estate

Tool | Pros | Cons | Pricing Model |

azakaw | End-to-end real estate compliance, Corporate compliance in one system; Native CBUAE, SAMA, DFSA, ADGM templates; Aqeen & Nafath Integration; Strong UBO/entity mapping Souce of Funds verification | Less brand recognition outside MENA/Africa than global incumbents | Usage-based / PLG, custom enterprise tiers Free trial |

Mozn FOCAL | Deep SAMA expertise; Yaqeen government database integration; strong KSA bank relationships | Limited presence outside GCC; corporate compliance module thinner than operational modules | Custom, contact sales |

Uqudo | UAE Pass and Yaqeen integration; strong document and NFC verification across 248 countries | Identity verification focus, not a full compliance workflow; no transaction monitoring | Custom, contact sales |

Sumsub | Fast onboarding for international buyers; broad document coverage; established in the UAE market | Governance and audit-trail depth are limited beyond verification | Per-verification ($1.35–$1.85) + monthly minimum Free trial |

Comply Advantage | Strong sanctions/PEP/adverse media screening; used across the UAE DNFBP sector | No native KYC or identity verification | From $99.99–$119.99/mo (Starter), custom Enterprise |

AMLOCK by Azentio | Enterprise-grade, UAE-headquartered vendor; case management and transaction monitoring built for regulated volume | Priced and built for banks and large financial institutions, heavy for a mid-size brokerage | From ~$52,000/year (Essentials) |

First AML | Strong entity-focused KYC for corporate and trust buyers is common in luxury GCC property | Higher cost; less flexible risk-model customisation | Custom, volume-based |

iComply | AI-powered KYB/KYC built around FATF-aligned obligations; low headline entry cost | Smaller reference base in the GCC than local specialists | From ~$1/entity/year (Essentials), tiered Plus plan |

Thirdfort | Built for UK conveyancers; useful for GCC firms with UK-linked buyers | UK-centric, not built around CBUAE or SAMA requirements | Custom, contact sales |

Smart Search | Used by 1,000+ UK property firms; a single platform for individual and business checks | UK-focused, limited relevance outside cross-border UK transactions | Subscription, custom |

Why real estate businesses need compliance software

Real estate keeps showing up as one of the sectors most exposed to money laundering, and in the UAE and Saudi Arabia, the legal room to treat compliance as optional has closed.

Compliance software exists to solve a specific, recurring set of problems for brokers, developers, and law firms:

Comply with local AML law: goAML registration, a named compliance officer, a business-wide risk assessment, customer due diligence, and suspicious transaction reporting are all required under the UAE's Federal Decree-Law No. 10/2025 and Cabinet Resolution No. 134/2025, and under Saudi Arabia's AML Law.

Avoid money laundering exposure: Screening buyers and transactions closes off property as an easy place to move large sums with little scrutiny, which is exactly why FATF keeps flagging the sector.

Avoid financial crime penalties: Documented due diligence holds up when a regulator audits the file. UAE AML fines run from AED 50,000 to AED 1,000,000 per violation, and the Ministry of Economy and Tourism has collected more than AED 130 million from DNFBPs since 2022.

Verify beneficial ownership: Mapping the individuals behind a corporate or trust buyer, not just the person signing the contract, is exactly what REGA's own guidance on beneficial ownership due diligence calls for.

Support cross-border buyers: FinCEN-style and UK AML obligations tied to a buyer's home jurisdiction sit on top of local rules whenever a buyer uses a UK entity, an offshore trust, or a non-GCC holding company.

Protect banking and lender relationships: Producing evidence that satisfies correspondent banks, escrow agents, and lenders on demand beats scrambling to reconstruct a file when one of them asks.

The common thread across all six: regulators and banks increasingly want proof, not a promise.

A brokerage that can only say "we checked their ID" has no answer when the question is "show me how you verified who actually owns that holding company."

How to choose real estate compliance software

Six criteria separate a tool built for how GCC real estate actually gets regulated from a generic KYC product with a real estate label on it.

Regulatory alignment: Look for native templates for CBUAE, SAMA, DFSA, and ADGM, not just generic KYC checks. Only these produce the business-wide risk assessment and goAML-ready reporting that inspectors actually ask for.

Source of funds verification is one of the most scrutinised obligations for real estate DNFBPs in the UAE and one of the least supported by generic KYC tools. Ensure for a structured workflow that collects documentation, assesses plausibility relative to the transaction value, records the risk decision, and logs who approved it. A bank statement on file is not compliance. A documented assessment is.

Beneficial ownership & entity mapping: Look for genuine KYB with UBO verification, not just individual ID checks. REGA's own guidance flags this specifically, and GCC property investment runs heavily through holding companies and trusts.

Government database integration: Search for native support for UAE Pass, Yaqeen, and Absher/Nafath. It turns a multi-day manual verification into a same-day check, and tools built for the region, like Uqudo and azakaw, support this out of the box.

Case files & audit trail: Look for exportable, inspection-ready reports rather than scattered screenshots. This is what a compliance officer needs to hand over in minutes when the Ministry of Economy or a Saudi regulator asks.

Cross-border capability: It's recommended to choose a tool with FinCEN-style and UK AML coverage layered on top of local rules. Necessary if any share of your buyer base is UK, US, or otherwise international.

Pricing that matches volume. Look for usage-based pricing instead of rigid annual licensing. Real estate transaction volume is irregular by nature, and per-transaction pricing tracks that better than a flat seat license.

The first two matter most: a tool that only satisfies those will get a small local brokerage through most regulator conversations.

Cross-border capability and flexible pricing start to matter once buyer volume grows or the buyer base becomes more international.

Compliance Software for Real Estate

Manage property transactions, legal documents, and stakeholder verifications from a single, intuitive platform that leverages the most advanced technology in the market, AI.

What are the best real estate compliance software?

The best real estate compliance software are azakaw, Mozn FOCAL, Uqudo, Sumsub, ComplyAdvantage, AMLOCK by Azentio, First AML, iComply, Thirdfort and SmartSearch.

azakaw

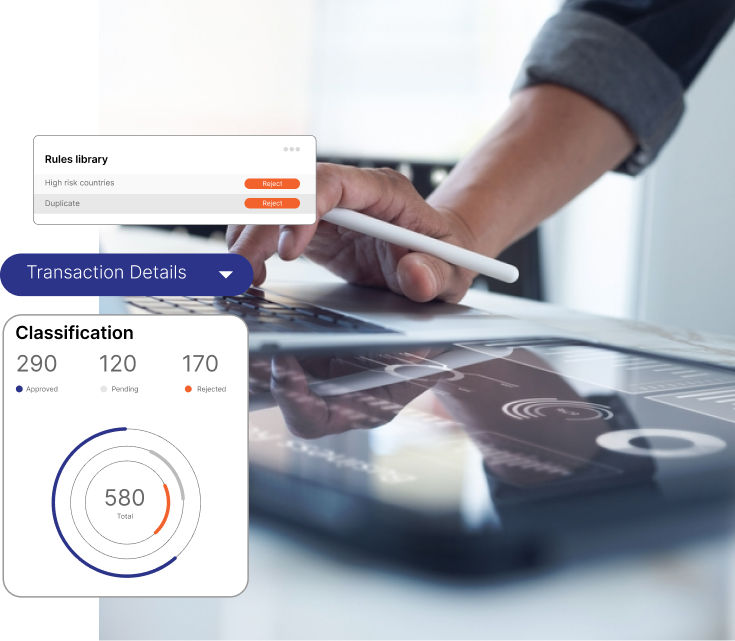

azakaw is a compliance operating system built inside j. awan & partners, a large GCC-based compliance advisory practice, covering digital onboarding (KYC/KYB), real-time AML screening, transaction monitoring, and corporate compliance governance in one platform.

For real estate specifically, its regulator-specific templates already cover CBUAE, SAMA, DFSA, and ADGM, and its KYB and UBO verification handles the holding companies and trusts common in GCC property deals.

Last but not least, azakaw was named an IDC Innovator in the IDC Innovators: Middle East Regulatory Technology Providers, 2026 report.

Pros:

Regulator-specific reporting templates for CBUAE, SAMA, DFSA, and ADGM, built for how UAE and Saudi DNFBPs are actually inspected

Source of Funds that collects documents, assesses plausibility, risk-rate, approve, and log. Every step captured automatically

Multi-party deal management in one place: buyer, seller, corporate entity, UBO

Strong UBO and public registry intelligence for verifying the company or trust behind a corporate property buyer

Audit-ready evidence packs and maker-checker approval workflows that produce inspection-ready reports on demand

Full KYC, KYB, AML screening, and corporate compliance governance in one system, covering both individual and corporate buyers

Usage-based commercial model that flexes with irregular transaction volume

Developed by compliance experts with +12 years of compliance experience in the GCC

Cons:

Less brand recognition among international buyers' home-market advisors than global names like Sumsub

Not purpose-built around UK-specific frameworks like HM Land Registry's Digital ID Standard for firms whose buyer base is mostly UK-linked

Pricing:

Usage-based, PLG-style commercial model with custom enterprise packages; no upfront licensing fees.

Best for:

UAE and Saudi brokerages, developers, and law firms that need goAML-ready compliance, strong beneficial ownership verification, and one system instead of stitching together a UAE Pass check and a separate screening tool.

End-to-End AML Compliance Tool

Manage property transactions, legal documents, and stakeholder verifications from a single, intuitive platform.

Mozn FOCAL

Mozn FOCAL is a compliance platform built in and for Saudi Arabia, recognised in Chartis FCC50 2025 and RiskTech100 2026, with Yaqeen government database integration and clients including AlRajhi Bank and STC Bank. Its KYC, AML screening, and transaction monitoring are built around SAMA expectations specifically.

Pros:

SAMA regulatory expertise, with compliance templates built around Saudi requirements rather than adapted from a global product

Yaqeen and other KSA government database integrations for fast, reliable identity checks

Strong relationships with major Saudi banks, which carry weight for developers and brokerages already working with those institutions

Cons:

Workflow customisation is limited, according to G2 reviews, which can matter for brokerages with non-standard approval processes

Geographic concentration in the GCC limits usefulness for firms with buyers outside the region, and it isn't positioned for Africa

Corporate compliance and governance capabilities are less developed than its operational (KYC/AML) modules

Custom pricing only, with no public free trial

Pricing:

Custom, available on request.

Best for:

Saudi-licensed brokerages and developers whose buyer base is concentrated in the Kingdom and who want a platform built specifically around SAMA expectations.

Read also: Mozn alternatives and competitors

Uqudo

Uqudo is an MEA-focused identity verification specialist with particularly strong coverage in the UAE and Africa, built around UAE Pass and Yaqeen integrations, NFC verification, and government database checks across 248 countries.

Pros:

UAE Pass and Yaqeen integration make individual buyer verification fast for GCC nationals and residents

NFC verification and document authentication reduce fraud risk on the identity side, specifically

Strong Africa coverage through local partnerships, useful for developers marketing to African buyers

Cons:

Identity verification is the core focus, without a full AML screening or transaction monitoring workflow built in

No corporate compliance module, so entity-heavy deals still need a second platform for governance

Implementation typically takes around 16 weeks, longer than some competitors

Very limited independent review presence at the time of writing (no G2 reviews yet), so most performance claims are vendor-reported rather than third-party verified.

Pricing:

Custom, available on request.

Best for:

Firms that specifically need best-in-class government-backed identity verification for individual GCC buyers and are comfortable pairing it with a separate AML and governance platform.

TIP: Read our post if you’re looking for Uqudo alternatives

Sumsub

Sumsub is a global identity verification and AML platform serving 4,000+ clients, with document coverage across 190+ countries. It has an established presence in the UAE market and is a common choice for developers and agencies marketing property to international buyers.

Pros:

Fast onboarding with high pass-through rates for international buyers unfamiliar with local verification processes

Broad document and country coverage, useful for developers selling to a genuinely global buyer base

Well-documented APIs that integrate reasonably easily into an existing CRM or transaction management system

Cons:

Case management and governance are basic, next to full compliance platforms, with no maker-checker approval chain

Not built around CBUAE, SAMA, or goAML-specific reporting requirements

Trustpilot reviewers report mid-contract fee increases, and some note verification delays during peak traffic periods

Pricing:

Per-verification pricing from roughly $1.35 (Basic) to $1.85 (Compliance tier with AML screening), with a monthly minimum of around $149.

Best for:

Developers and agencies with a genuinely international buyer base that need broad document coverage, with GCC-specific compliance handled elsewhere.

Related content: Sumsub alternatives and competitors

ComplyAdvantage

ComplyAdvantage is an AI-native AML screening and monitoring platform used across the UAE's DNFBP sector, useful for firms that already have identity verification handled and need stronger sanctions, PEP, and adverse media screening layered on top.

Pros:

Reported reductions in false positives and faster review cycles after automation

Transparent entry-level pricing plus a startup program (ComplyLaunch) offering extended free access to eligible early-stage companies

Reliable API, frequently mentioned as a strength in reviews

Cons:

No native KYC or identity verification, so it needs to sit on top of a separate ID verification tool

Not built around goAML-specific reporting or GCC regulator frameworks

Some reviewers report noisy false positives in adverse media matching

Pricing:

Starter plan from roughly $99.99 to $119.99 a month for 100 entities; custom Enterprise pricing for higher volume.

Best for:

UAE or Saudi firms that already have an identity verification process and need to add or upgrade sanctions and PEP screening specifically.

AMLOCK by Azentio

AMLOCK, one of the best AML & KYC software in the UAE, formerly TCS AML, is an enterprise AML platform from Azentio, a UAE-headquartered vendor, with rule sets covering 40+ countries and full case management and transaction monitoring capability built for regulated financial-sector volume.

Pros:

Built and supported from the UAE, with enterprise-grade case management and transaction monitoring

Dynamic risk rating, sanctions screening, and watchlist checks in one platform

Proven at bank and large financial institution scale, which matters for master developers or large brokerage groups with bank-level transaction volume

Cons:

Implementation and configuration are time-consuming and resource-heavy, and pricing and complexity are calibrated for banks and major financial institutions, not a typical mid-size brokerage

Limited public review visibility on G2, Capterra, and Trustpilot compared to more consumer-facing platforms, which makes independent verification of performance claims harder

Can be over-featured and expensive relative to what a smaller brokerage or developer actually needs

Pricing:

From approximately $52,000/year for the Essentials package, usage-based beyond that.

Best for:

Large developers, master developers, or brokerage groups with transaction volume closer to a financial institution's than a typical agency's.

First AML

First AML's Source platform focuses on entity-heavy KYC and CDD, with a "Met In Person" feature letting agents scan IDs on a mobile device during in-person meetings, which suits the high-touch relationship style common in GCC luxury property sales.

Pros:

Strong fit for corporate and trust buyers, common in high-value GCC property transactions structured through holding companies

Met In Person and remote webform options cover both in-person meetings and remote international buyers

Built for ongoing monitoring, not just a one-time check at onboarding

Cons:

Reviewers note the cost sits on the higher end of the category

Not built around GCC-specific regulator frameworks or government ID integrations like UAE Pass or Absher

Pricing:

Custom, volume-based, with an entry plan built around a minimum of roughly 400 individuals or 100 complex entities a year.

Best for:

Firms handling a high proportion of corporate or trust buyers who need strong entity-level due diligence alongside in-person verification.

iComply

iComply is a modular AI-powered platform covering KYC, KYB, and AML, built with FATF-aligned obligations in mind and positioned around automating buyer and seller verification for property transactions internationally.

Pros:

Built explicitly around FATF-aligned real estate compliance obligations rather than adapted from a generic KYC product

Low headline pricing, with entry costs cited as low as roughly $1 per entity per year on the Essentials tier

Coverage across 195 countries suits firms with a genuinely global buyer base

Cons:

Smaller reference base in the GCC, specifically, than regional specialists like Mozn FOCAL or Uqudo

Not built around CBUAE, SAMA, or goAML-specific reporting workflows

Pricing:

Tiered, from roughly $1/entity/year (Essentials) up to a Plus plan with expanded automation and 195-country coverage.

Best for:

Firms that want a cost-efficient, FATF-aligned platform for international buyers alongside GCC-specific compliance handled through a regional tool.

Thirdfort

Thirdfort is built specifically for UK legal, property, and accountancy compliance teams, meeting HM Land Registry's Digital ID Standard and the Companies House identity verification standard. It's relevant to GCC firms mainly when a UK-linked buyer or a dual UAE-UK transaction is involved.

Pros:

Reports typically return in under a minute, with source-of-funds checks built in

Meets HM Land Registry and Companies House identity standards directly, useful for GCC developers selling to UK-resident buyers

ISO 27001 certified, with consistently praised customer support

Cons:

Built entirely around UK requirements, with no CBUAE, SAMA, or goAML alignment

Pricing isn't public and requires a sales conversation

Pricing:

Custom, available on request.

Best for: GCC brokerages and developers with a meaningful share of UK-linked buyers who need UK-standard checks alongside their local compliance stack.

SmartSearch

SmartSearch is a long-established UK AML platform used by more than 1,000 property firms and a third of the UK's top 200 law firms, combining sanctions, PEP, and adverse media screening with individual and business verification.

Pros:

Real-time checks that complete in seconds, with automatic escalation to enhanced due diligence on sanctions or PEP matches

One platform for both individual and business/entity checks

Fast integration, reportedly completed within 24 hours in many cases

Cons:

Built for UK-regulated firms, with no visible alignment to CBUAE, SAMA, or GCC-specific reporting

Limited relevance unless your transaction flow specifically includes UK-linked buyers or entities

Pricing:

Subscription-based; custom quote required.

Best for:

GCC firms handling a UK-linked portion of their buyer base who want an established UK platform to cover that specific exposure.

How to choose the right real estate compliance software

The right choice depends mainly on transaction scale and how international your buyer base is:

Boutique UAE brokerage or solo Saudi-licensed agent, mostly local buyers: Prioritize goAML-ready reporting and fast government ID checks, without enterprise-scale commitment. azakaw's usage-based pricing covers this, and Uqudo is worth a look specifically for its UAE Pass and Yaqeen integration.

Mid-sized developer or brokerage group, mix of GCC nationals, expats, and some international buyers: Prioritize regulatory depth plus the ability to handle holding companies and trusts. azakaw or Mozn FOCAL cover the regulatory side well, with First AML worth adding if trust-structured deals are common.

Large developer, master developer, or multi-country GCC group with real international volume: Prioritize full regulatory depth (CBUAE/SAMA/DFSA/ADGM) plus cross-border reach. azakaw covers the regulatory coverage and governance, layered with Thirdfort or SmartSearch for UK-linked transactions, or iComply for broader FATF-aligned coverage.

Why azakaw is the best real estate compliance software

The UAE and Saudi Arabia didn't tighten real estate AML rules as a formality.

Federal Decree-Law No. 10 of 2025, the follow-up Cabinet Resolution, and REGA's beneficial ownership guidance all point at the same gap: brokers and developers who can verify a buyer's passport but can't show who actually stands behind a corporate purchase or produce a risk assessment on demand.

azakaw's KYB and UBO verification map that ownership structure directly, and its evidence layer ties KYC, screening results, and approvals into a single case file that a compliance officer can hand over during an inspection instead of reconstructing after the fact.

The impact shows up in the numbers azakaw clients report:

5x faster onboarding compared to manual, spreadsheet-based verification

75% faster KYC/KYB approvals, cutting the time between an accepted offer and a signed, compliant contract

80% drop in false positives and screening reviews, so compliance officers spend less time chasing dead-end alerts

85% faster regulatory reporting generation, turning a Ministry of Economy or SAMA inspection request into a same-day response instead of a week-long scramble

30% lower annual compliance costs from automation replacing manual document handling and re-keying

98.5% accuracy in verification, alongside a 65%+ reduction in fraud exposure across onboarding

Tony Hallside, Managing Director of STP Partners Limited, a prime brokerage firm regulated by the DFSA in DIFC, described the shift after moving to azakaw:

"We've gone from spending countless hours on compliance to having a system that practically runs itself. The platform isn't just meeting our needs; it's evolving alongside them.

That regulator-specific depth is the part most global platforms don't have. azakaw's templates already align with CBUAE, SAMA, DFSA, and ADGM requirements, which means a Dubai brokerage, a Riyadh developer, or a DIFC-based real estate fund isn't retrofitting a generic KYC tool to fit local reporting expectations.

And because the platform is usage-based rather than seat-licensed, it scales with the reality of real estate transaction volume, busy in one quarter and quiet the next, instead of charging like a bank-grade platform built for steady daily volume.

International reach matters too, since a meaningful share of GCC property buyers come from outside the region.

azakaw's coverage extends across MENA and Africa from eight regional offices, so a corporate buyer with a South African shareholder or a European correspondent banking relationship doesn't fall outside what the platform can screen and document.

Compliance does not run itself through manual processes, disconnected tools, and spreadsheet-tracked SoF assessments. It runs itself when the platform is built to capture the whole programme, from first identity check to the last document in the five-year retention window.

End-to-End AML Software

Streamline compliance from identity and business verification to SOF, UBO mapping and AML transaction monitoring, reducing costs and complexity so you can scale with confidence.

FAQ

Do real estate agents in the UAE need AML software?

Yes. Real estate brokers and agents are classified as Designated Non-Financial Businesses and Professions under UAE law, which means goAML registration, a named compliance officer, customer due diligence, and suspicious transaction reporting are mandatory.

Are Saudi Arabian real estate brokers required to do AML checks?

Yes, real estate agents need to do AML checks, since they are classified as DNFBPs under Saudi Arabia's AML Law and supervised by the Ministry of Commerce. The Real Estate General Authority has also published specific guidance on customer due diligence and beneficial ownership verification for real estate brokerage services.

What is goAML, and do I need to register?

goAML is the UAE's platform for suspicious transaction and activity reporting, managed by the Ministry of Economy and Tourism's AML department. Real estate brokers and agents classified as DNFBPs are required to register on goAML and file reports through it as part of their AML obligations.

What is the best real estate compliance software in 2026?

It depends on where your buyers are. For a platform covering CBUAE, SAMA, DFSA, and ADGM requirements in one system with strong beneficial ownership verification, azakaw is the strongest overall fit for UAE and Saudi brokerages.

How much does real estate compliance software cost in the GCC?

Pricing varies by scope. Identity-focused tools like Sumsub charge per verification, roughly $1.35 to $1.85. Full-lifecycle platforms like azakaw use usage-based pricing that scales with transaction volume. Enterprise-grade platforms built for banks, like AMLOCK, start around $52,000 a year and are generally too heavy for a typical mid-size brokerage.

Do I need separate software for individual buyers and corporate or trust buyers?

Not necessarily, but many identity-verification-only tools handle individuals well and corporate structures poorly.

Given how much GCC property investment runs through holding companies and trusts, and REGA's specific guidance on beneficial ownership verification, look for a platform with genuine KYB solution and UBO mapping, such as azakaw or First AML, rather than assuming an individual-focused tool will cover it.

Is Source of Funds verification mandatory for real estate transactions in the UAE?

Yes. UAE AML obligations for real estate DNFBPs require assessment of the client's financial background and source of funds as part of the CDD process.

Conclusion

The UAE and Saudi Arabia have both closed the gap on real estate AML oversight, and neither is loosening it.

Brokers and developers now need to show their work, not just pass a buyer's ID through a scanner.

For UAE and Saudi brokerages, developers, and law firms that want one platform for individual and corporate buyers, CBUAE/SAMA/DFSA/ADGM-aligned reporting, and an audit trail that holds up during a Ministry of Economy inspection, azakaw is the strongest real estate compliance software pick for 2026.

Compliance Software for Real Estate

azakaw modernises real estate transactions, making it easy to stay compliant. Request documents, verify parties, and collect signatures through a secure, user-friendly portal.

Related articles:

Sources

UAE Ministry of Economy and Tourism guidance, Cabinet Resolution No. 134 of 2025, Federal Decree-Law No. 10 of 2025

REGA guidelines on beneficial ownership in real estate brokerage, Saudi Arabia's AML Law

G2

Capterra

Vendor pricing pages